Situation Brief: Jet2 plc (AIM:JET2)

If Booking.com and Ryanair had a love child, it would look something like this

This is the first post in my Taking AIM series, where I go through AIM-listed businesses to see if I can find any nuggets of value.

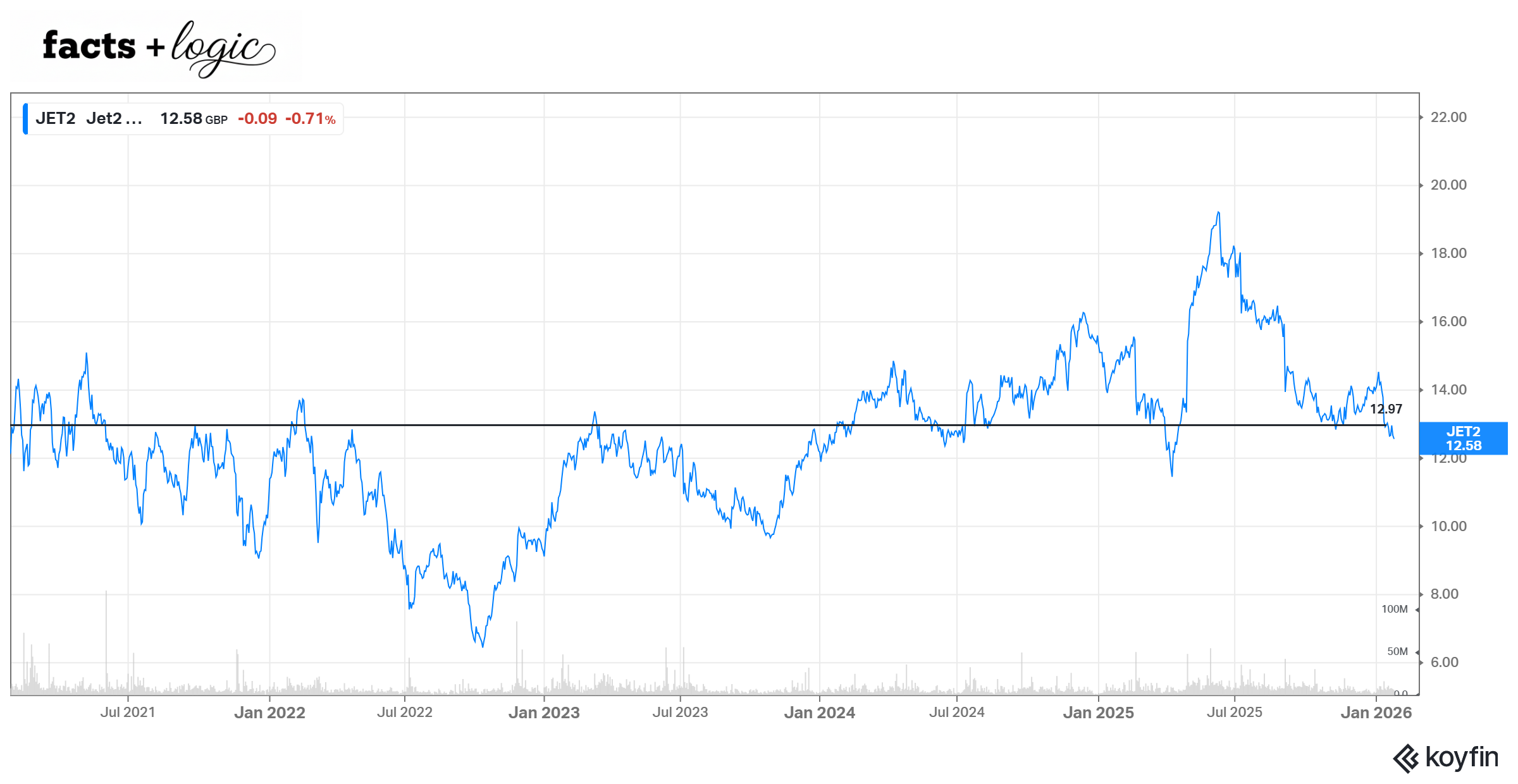

According to Koyfin, the largest stock on the AIM by market cap is Jet2 plc (AIM:JET2). There are currently 197.8m shares outstanding, trading at £12.60 per share, giving a market cap of £2.5bn.

I see Jet2’s grey and red planes whenever I travel home via Leeds Bradford Airport. That’s as good a reason as any to take a look.

Position & Transparency Report

Ticker: AIM:JET2

Current Position: No Position

Recent Activity: None

Blackout Status: The author certifies that no trades have been executed in this security within the one-day pre-publication window. Per the Facts + Logic protocol, a two-day post-publication blackout is now in effect.

Post-Publishing Edits: Edited out a couple of typos.

Jet2 is the largest package holiday operator in the UK, capturing 20% share of the market. It is generally loved by both customers and employees. The business is vertically integrated, owning its airline but not the hotels/resorts.

Jet2 has spent 20 years growing their market share, reinvesting basically all cash flow at 15%+ ROICs, and created 15% TSRs in the process.

JET2 currently trades around £12.60, which is 6x consensus FY26 earnings (yearend March 31st). It peaked at £19.40 in June 2025.

Risk/reward

Bottom Line: ~0% downside; +80-120% upside.

Jet2 appears to have ~£5.80 in distributable net cash (net of debt) per share on the balance sheet. Excluding net cash, the stock trades at £6.80 or 4x unlevered EPS of ~£1.70.

The balance sheet also shows £8 per share in owned planes, so the business is trading below the depreciated value of the owned fleet. The combo of a holiday booking business and an airline fleet has delivered mid-teens ROICs for Jet2 in the past.

At present, this fleet is expanding and getting more efficient. Jet2 has 135 planes in service. 23 are Airbus A321neos. The rest are mostly 737-800s. Jet2 has committed to owning 146 neos and leasing 9 more by Summer 2035. They are retiring 737-800s as the larger, more fuel efficient neos come online. A 1:1 replacement of Airbuses for Boeings would grow available seat capacity 4% CAGR over the next decade.

This capacity growth will be somewhat frontloaded: it is set to rise ~9% from Summer 2025 to 2026. This year’s expansion will be focused on expanding their presence at London Gatwick Airport. However, this new inventory will not be fully utilized at full price until the 2027 summer season. Mr. Market is treating this temporary margin pressure as a permanent state of affairs.

Netting off various assets and liabilities, liquidation value appears to be ~£12.50. Downside looks limited.

A business earning 15% on its capital with a 4% growth rate and a 9.4% cost of capital produces a stock worth ~13x unlevered EPS plus net cash. For Jet2 that’s £28 (+121%). In the past, Jet2 has averaged a 10x P/E, so that’s £23 (+80%).

What matters at £12.60?

£12.60 is about right if:

The competitive advantages (and excess returns) enjoyed by the existing fleet and holiday business are going away completely, and future investments in capacity-led growth will add no value, OR

The industry is undergoing a structural decline in margins that participants cannot rectify through price adjustments.

If research gives reason to believe in one of the above, we’ll just move on to something else.

Key questions

If the answers to the questions below are is “no”, then Jet2 is definitely mispriced:

Is their competitive advantage going away?

Are new / growing UK package holiday competitors driving down prices?

Are new / growing competitors stealing market share?

Are competitors’ customer satisfaction scores improving, indicating declining competitive position?

Are Jet2’s customer satisfaction scores declining, indicating current brand damage?

Are employees highlighting falling operating standards, indicating future brand damage?

Are resort vendors demanding higher prices, indicating declining take rates?

Is Jet2 more exposed than peers to fuel, regulatory, or other cost increases, so that raising prices to maintain margins would cause declining volume?

Is there a structural decline in industry margins:

Are marketing and advertising costs accelerating across the industry, indicating excess capacity?

Are peers’ management’s also talking about “temporary” margin pressure as they absorb new aircraft deliveries?

Do peers’ management’s also expect aircraft deliveries to accelerate faster than volume growth?

Does it all hinge on improving capital allocation?

Even with the same capital allocation and shitty airline multiples, the total value would be ~£14.70 (+17% upside)

If management doesn’t make a dent in the cash balance, then the cash is negative leverage. Equity holders pony up cash pound-for-pound and it diminishes their returns.

Assume Jet2 can earn £1.70 in operating EPS sustainably, and the market thinks that’s only worth 6x, or £10.20. (This is where the market is pricing European airlines at the moment).

Assume also that Jet2 will perpetually carry £2.8bn in net cash earning 4%, which adds £0.43 in EPS. Equity holders finance that cash balance, so the market values it at the required return, or 9.4%. That’s adds £4.50 in value.

Even with no change in capital allocation policy and a perpetually low airline multiple, the total value would be ~£14.70 (+17% upside). If that’s how this goes down, fine; we live to fight another day.

What next?

First stock reviewed and it’s worth doing some proprietary digging. That’s fortuitous.

If you want to keep up with the story as I attack these questions, go ahead and subscribe below.

Hi, how should we think about their future capex commitments in the form of airplane orders?