Situation Brief: Agronomics Ltd (AIM:ANIC)

Mr. Mellon knows something I don’t. But I’ve got better things to do with my time.

This is my second Situation Brief on AIM-listed companies. Here I look at Agronomics Ltd (AIM:ANIC), a listed venture capital firm (equity market cap = £63m) investing in precision fermentation and cultivated proteins start-ups. None of its portfolio companies is cashflow positive.

As of December 2025, ANIC had 1,015,905,830 shares outstanding. The investment portfolio’s carrying value was £138m. They show £2.2m in cash, so they are basically fully deployed. They are debt-free, so net assets were £140m.

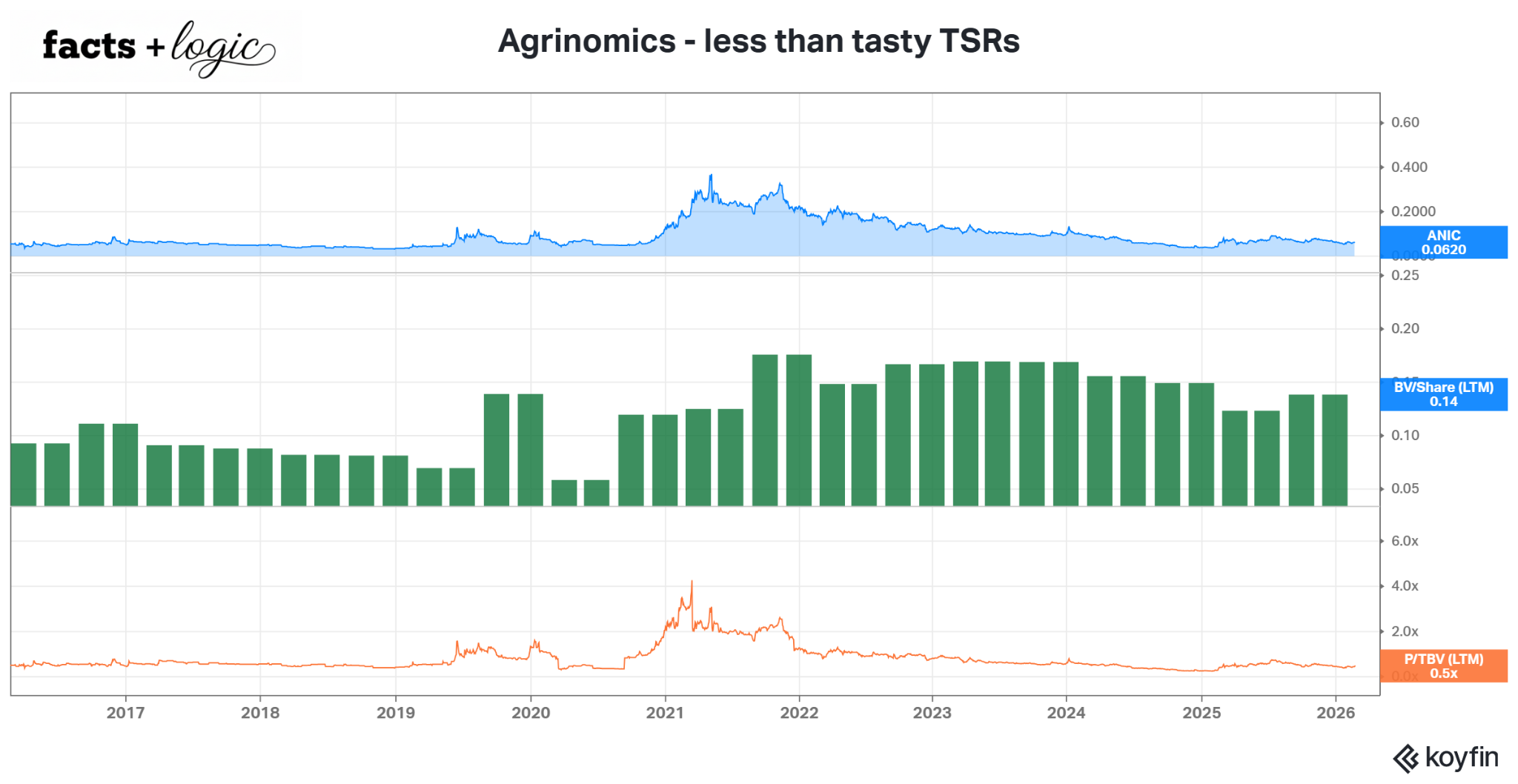

As of December, NAV of 13.8p compares with ANIC shares trading at 6.2p, or 45% of book value.

Position & Transparency Report

Ticker: AIM:ANIC

Current Position: No Position

Recent Activity: None

Blackout Status: The author certifies that no trades have been executed in this security within the one-day pre-publication window. Per the Facts + Logic protocol, a two-day post-publication blackout is now in effect.

Post-Publishing Edits: None

Why Look?

Agronomics screens as negative EV, i.e., equity < net cash. This is because the investment portfolio is included in cash and investments.

In reality, assets total £140.2m, substantially all of which is the investment portfolio. There is no debt. The market cap of the equity is £63m gives a P/B of 0.45.

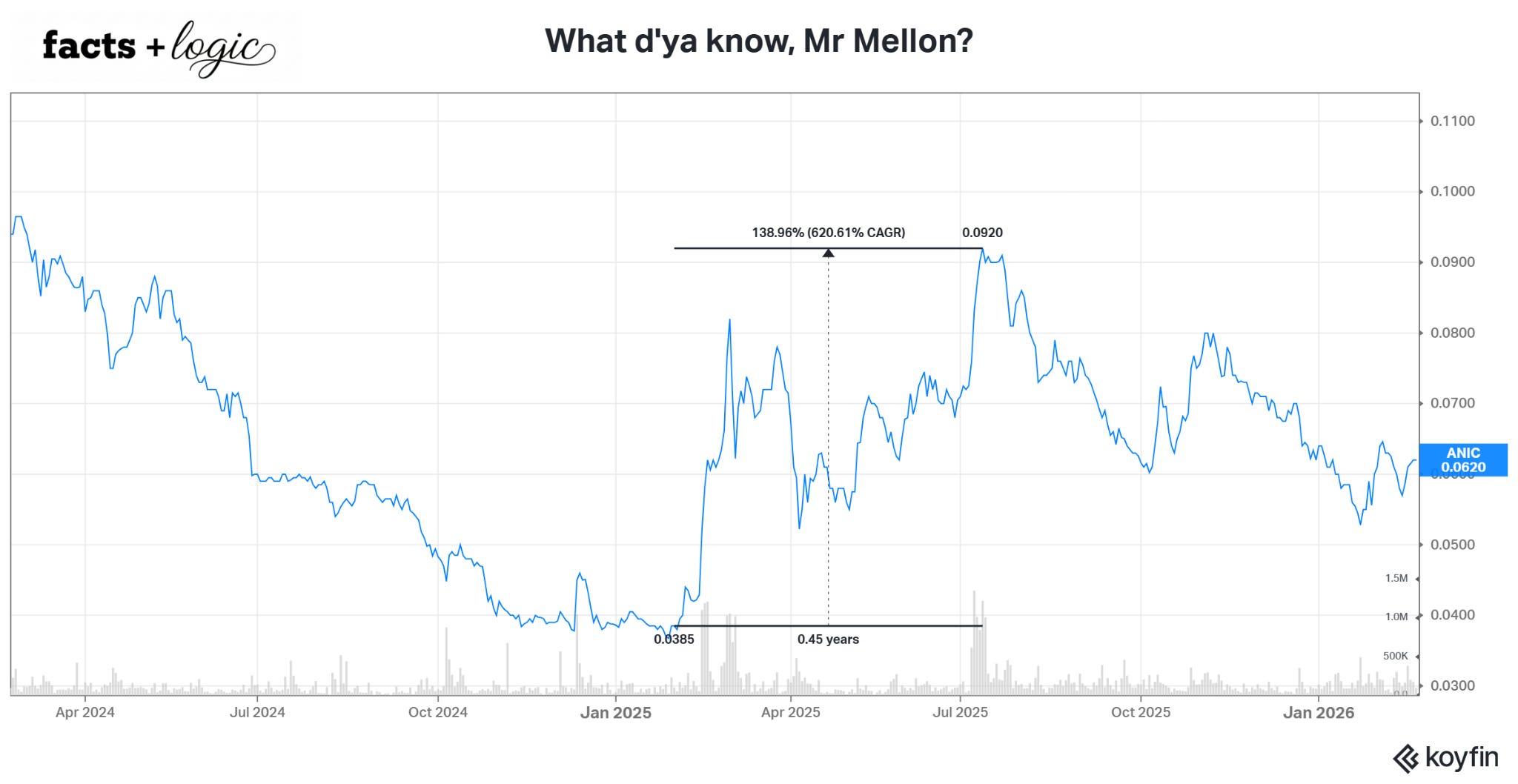

The Executive Chairman, Jim Mellon, seems to be running the show. He recently purchased 2.16m shares at 6p, putting £130k more of his own money at risk. His holdings total 15% of the company.

The last time Mr. Mellon bought shares was Feb 4th 2025 (RNS) at 3.7p. Just days before, ANIC had made a follow-on investment (RNS) in their largest holding, Liberation Bioindustries Inc. The stock was up 130% over the next 5 months (below) before dropping back from 9.2p to 6.2p.

This makes me wonder what Mr. Mellon is up to this time. The last announcement was a £1.5m follow-on investment (RNS) in Australian cultivated dairy protein company, All G. ANIC has put in £8.9m and owns about 5% of the company, which isn’t significant to ANIC’s valuation. Hmmmm…?

The Business

Agronomics is a listed venture capital firm investing in private businesses in the precision fermentation and cultivated proteins niches. Agronomics Limited is a Company domiciled in the Isle of Man and listed on the AIM. They position themselves as a leading investor in Clean Food. Economically ANIC is a set of interests in early stage businesses with a common theme: using cellular agriculture to monetize the increasing demand for protein ingredients.

FY25 Annual Report: The Company’s strategy is to create value for Shareholders through investing in companies that operate in the nascent industry of cellular agriculture, which are environmentally friendly alternatives to the traditional production of meat and plant-based sources

Some portfolio companies are in production technology, like Liberation Bioindustries. Others are developing innovative proteins, like Blue Nalu and SuperMeat.

The top 10 investments make up 85% of the £140m portfolio value at December 31, 2025, with Liberation Bioindustries Inc (biomanufacturing/precision fermentation) constituting 25%, Blue Nalu Inc (cultivated tuna) constituting 12%, SuperMeat (cultivated chicken) constituting 11%. Solar Foods constitutes 5% and IPOd at the end of 2024 (HLSE:SFOODS).

Agronomics’s assets are substantially all investments. They are more or less fully invested at this point. Agronomics has no debt or other material liabilities. Investments are carried at the most recent transaction value, i.e., the last funding round valuation. They are not re-marked for operational progress or setbacks. Therefore, the portfolio carrying value masks both upside and downside value differentials.

So investors will make money if the portfolio turns out to be worth more than market implied value, which is 0.47x carrying value, after deducting the ongoing management costs of the fund.

TSRs and ROICs

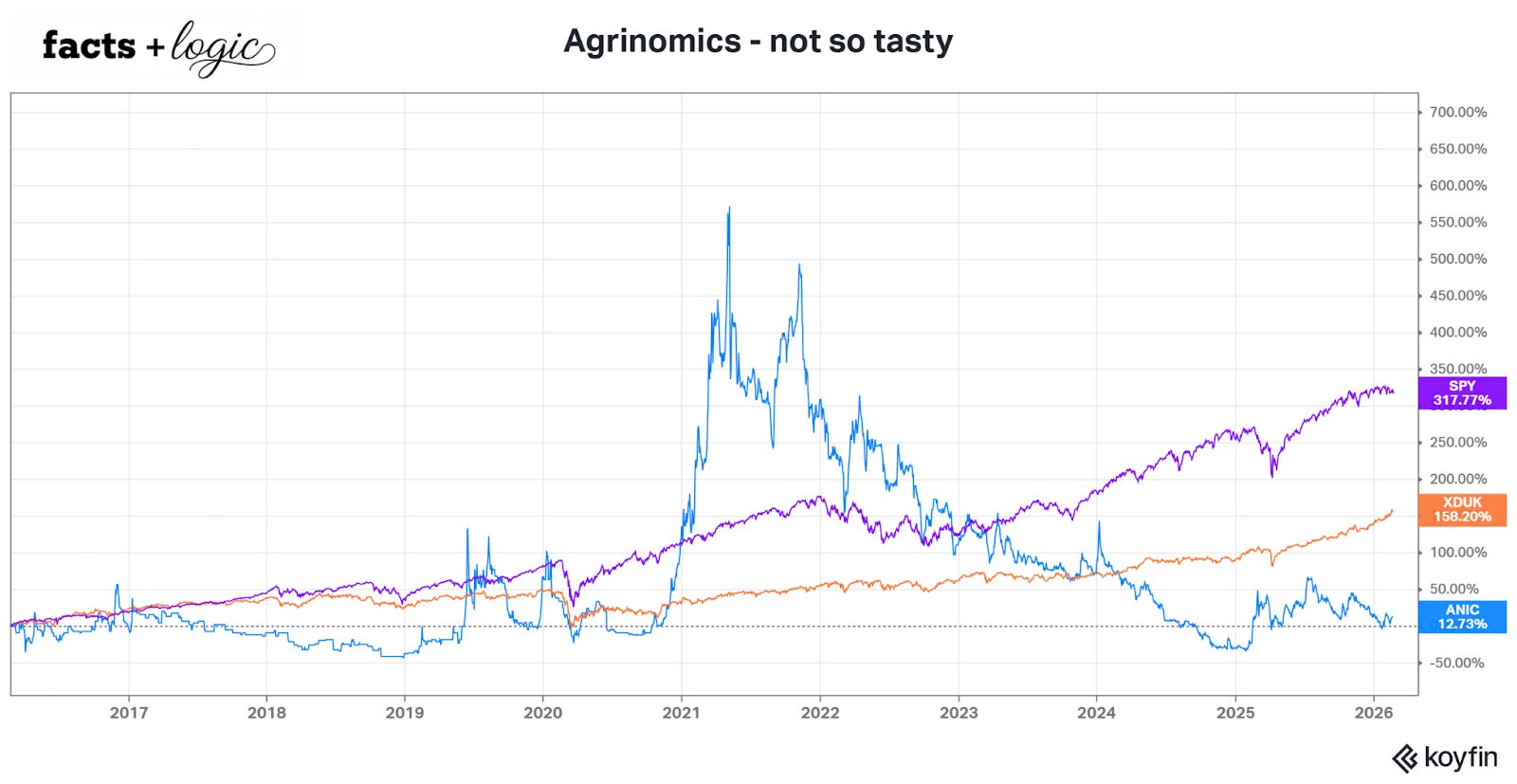

Agronomics has not delivered for investors so far. Book value has compounded at 4.2% CAGR over the past decade. With the decline in P/B, the stock has returned 1.2% TSR:

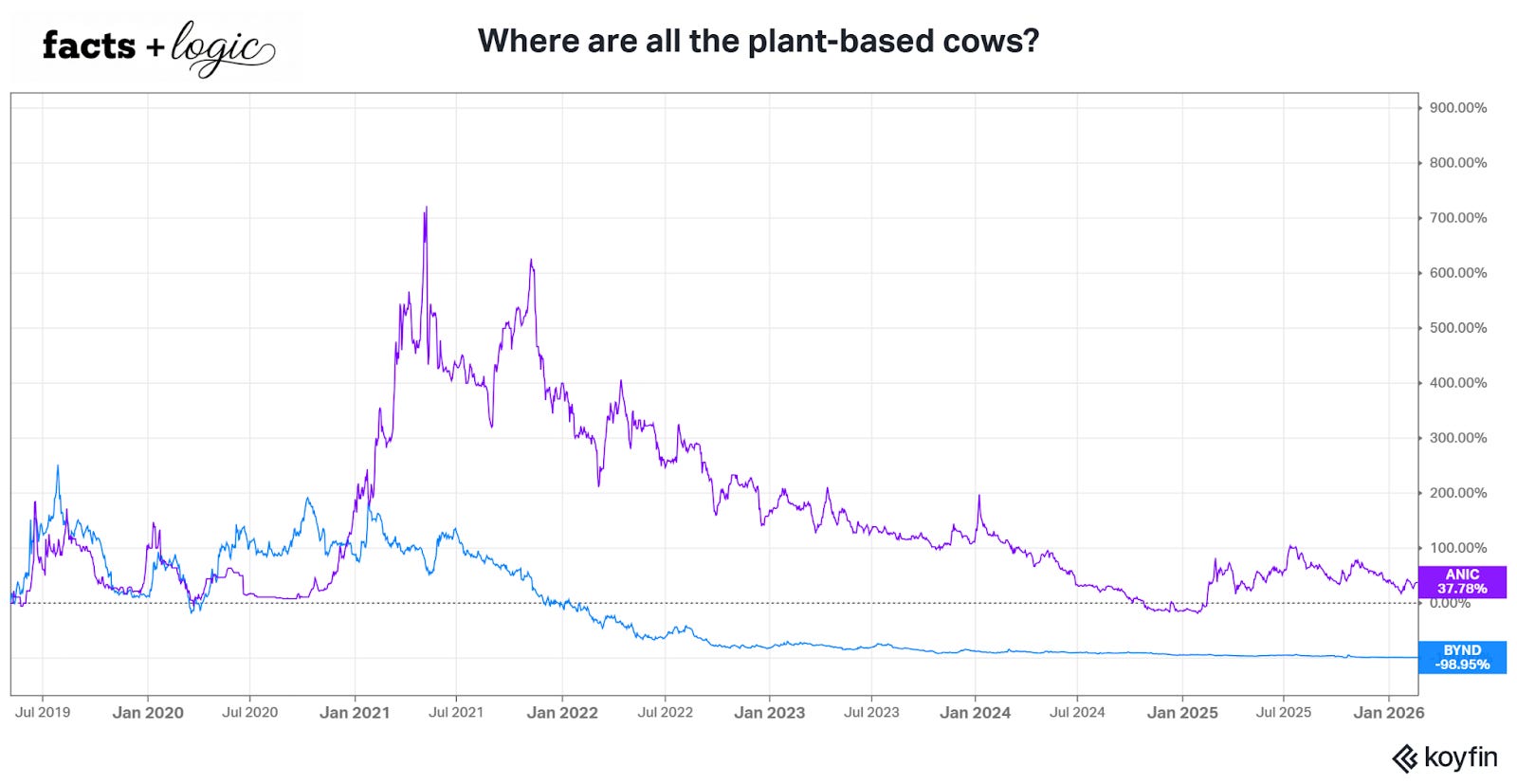

The big run up in 2021 was when plant-based protein companies, like Beyond Meat (NASDAQ:BYND) and Impossible Foods (private), were having a moment. We were going vegan. But then we actually tried the expensive burgers and promptly stopped buying them. Investors have thrown up their meat alternatives and tossed ANIC into the compostables bin.

BYND has not been able to scale profitably and the stock has been a wipeout:

The Opportunity?

This much negativity is usually a good thing. Impossible Foods and Beyond Meat may be nothing-burgers but there is high demand for protein-enhanced… everything. I can imagine that there could be as-yet unmet demand for sustainably-produced protein ingredients. So maybe there’s something tasty hiding in here.

When I look at ANIC, the first thing I think is, “what do I get if I buy this thing?”

Here’s the latest portfolio disclosure:

Investments in Liberation Bioindustries Inc constitute 25% of ANIC’s portfolio. Given the multi-bagger or nothing nature of early stage investments, such a large allocation to one name could determine the performance of the whole portfolio. It’s entirely conceivable that Liberation could be a 10-bagger for Agronomics. All else equal, that would triple the value of the portfolio, making ANIC a triple.

Rather than producing novel animal protein alternatives, Liberation is a firm of facility engineers and operators. There is (supposedly) a lack of industrial capacity to produce novel proteins at commercial scale. The start-ups inventing the proteins can’t fund manufacturing facilities large enough to reach commercial viability. There’s a chicken-alternative or egg-alternative problem.

Liberation intends to fill that gap. Their model is to design, build, and operate industrial facilities that produce specific classes of novel protein (e.g., dairy or egg alternatives, pharmaceutical or industrial products, etc.) at a scale that brings price parity with animal protein. They will operate these facilities as a contract manufacturer.

They are in the late stages of building a flagship facility at Midwest Industrial Park in Richmond, Indiana. Their website claims 600,000 litres of fermentation capacity and operations commencing in 2026. You can find progress pictures on their LinkedIn here. They claim that 50% of that capacity is presently or soon to be contracted:

Press Release: The company has made significant strides in customer acquisition, with well over 50 percent of nameplate capacity at the Richmond plant under contract or in late stages of agreements. The company has announced it will produce commercial scale volumes of Vivitein™ BLG, a dairy protein for Dutch ingredients startup Vivici. In addition, Liberation Bioindustries announced a strategic partnership with Topian, NEOM’s food company, to design and develop an advanced precision fermentation facility in Saudi Arabia. Planning for this project is underway.

The issue is… I have no idea how to value an early stage investment in a private company without any access to their accounts.

What matters at 6.2p?

6.2p could be an appropriate price for ANIC if:

The true value of the investments ANIC made in prior years (during a meatless-future hype cycle) is ½ the carrying value posted on the balance sheet, OR

The PV of fees due to ANIC’s fund managers will consume half the value of the portfolio.

Conversely, 6.2p could be the wrong price for ANIC if:

ANIC’s 25% investment in Liberation Bioindustries Inc worth 10x its carrying value. The rest of the portfolio could go to zero but the NAV would still be 70% more than the current price.

Bottom Line: For Agronomics to be an investable opportunity, I would need to believe that ANIC’s 25% position in Liberation Bioindustries will soon be worth much more than their entire £138m portfolio. That means it needs to be at least a 4-bagger in fairly short order.

I don’t know how to research the economics of Liberation’s private business, especially in an unproven industry. So that’s a non-starter. Additionally, I doubt it’s worth my time. Valuations of capital intensive manufacturing businesses are constrained by the ROIC of their manufacturing capacity, which is rarely anything to get excited about. Manufacturing is not scalable like software where product-market fit can be established and then you sell, sell, sell to produce vast amounts of FCF. Sudden, massive increases in the EV of manufacturers are rarer than… plant-based cows.

What next?

If you can figure out the true economic value of ANIC’s Liberation investment, this could be a winner for you. I can’t. I can only speculate on why Mr. Mellon is buying right now. He knows things I don’t and can’t easily find out.

I’m moving on to other things.