Research Note: Jet2 plc (AIM:JET2)

Ok business with a tasty yield. I nibbled on it a little. More to come.

In the Jet2 Situation Brief, I observed that JET2 would be mispriced if the answer to both of the following questions was “no”:

Is their competitive advantage going away?

Is there a structural decline in industry margins?

There is a third question, which I should have included:

Will the cash on the balance sheet be reinvested at below-historical ROICs?

This research note attempts to answer the last of these. I will address the others shortly in a follow-up.

Position & Transparency Report

Ticker: AIM:JET2

Current Position: Long

Recent Activity: Bought on Feb 2nd, 2026 at £12.51

Blackout Status: The author certifies that no trades have been executed in this security within the one-day pre-publication window. Per the Facts + Logic protocol, a two-day post-publication blackout is now in effect.

Post-Publishing Edits: Adjusted valuation (down) for increased maintenance

Takeaways

Jet2’s distributable cash is less than previously hoped

Operating cash brings estimated ROIC down to ~13% vs. the ~15% previously identified

I think Jet2 earns ~9% ROIC on new A321neo deliveries out of the gate

Base case Economic EPS of £2.25 implies yield of ~18%

In the first post, I noted that Jet2 is sitting on roughly one fuck ton of cash. What they do with this matters. Simply put, is that fuck ton is worth more or less than a fuck ton?

Will the cash be reinvested at lower than historical ROICs?

In short, sort of. The accounting ROICs are inflated by an aged fleet. There is an extensive capex plan to add 155 A321neo planes through 2034, largely replacing the aged 737-800NG fleet. At current profit levels and plane prices, these new planes generate ~9% ROICs out of the gate.

That seems low. Does it matter? Not much. They plan to finance half the A321neo program with debt, currently available at <5%. That gives a WACC of ~7.5%, so the neos are still value-additive for shareholders and the thing is trading close to asset value. However, given the low returns, stratospheric future valuations probably depend on declining interest rates and/or moderating competition.

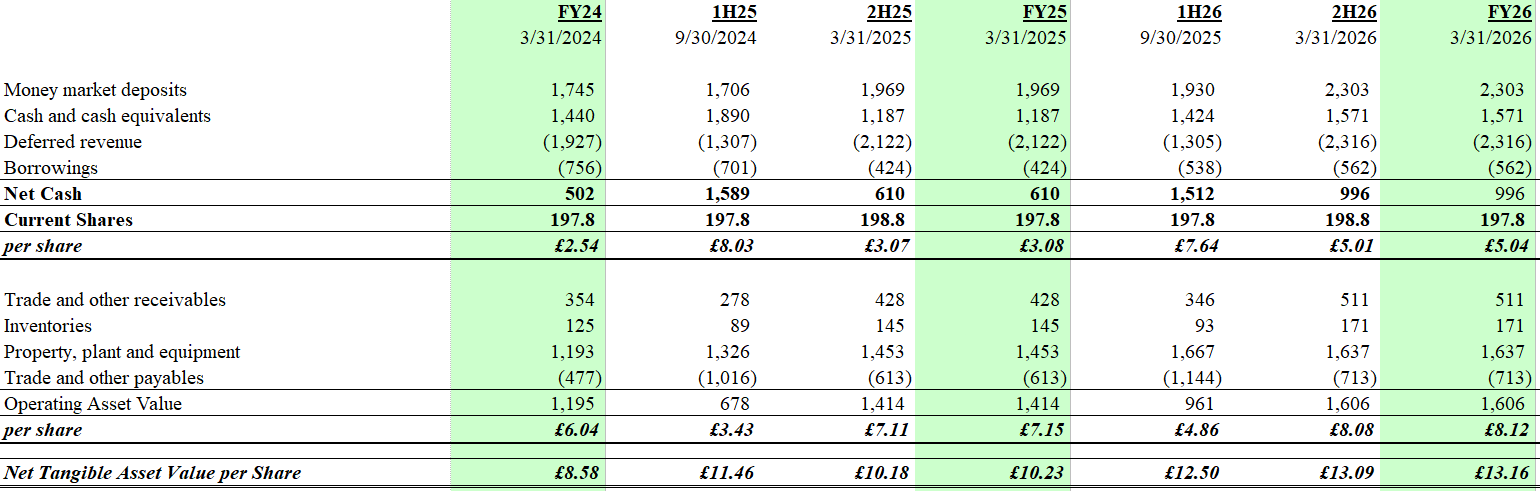

Distributable cash & current ROIC

On their last call, Jet2 provided a minimum yearend liquidity requirement: £600-700m in cash plus £500m in undrawn revolver capacity. They don’t expect this to grow with the business. I think they’ll end the year in March 2026 with ~£3.8bn in cash on the balance sheet and net tangible asset value over £13 per share:

Allocating £700m to operating cash, that leaves £700m in excess cash at yearend (below). That’s enough to buy back 28% of the business at today’s prices. I don’t think they will buy back that much stock straight away. They have deliveries of planes coming up and they’ll want to keep their financing options open.

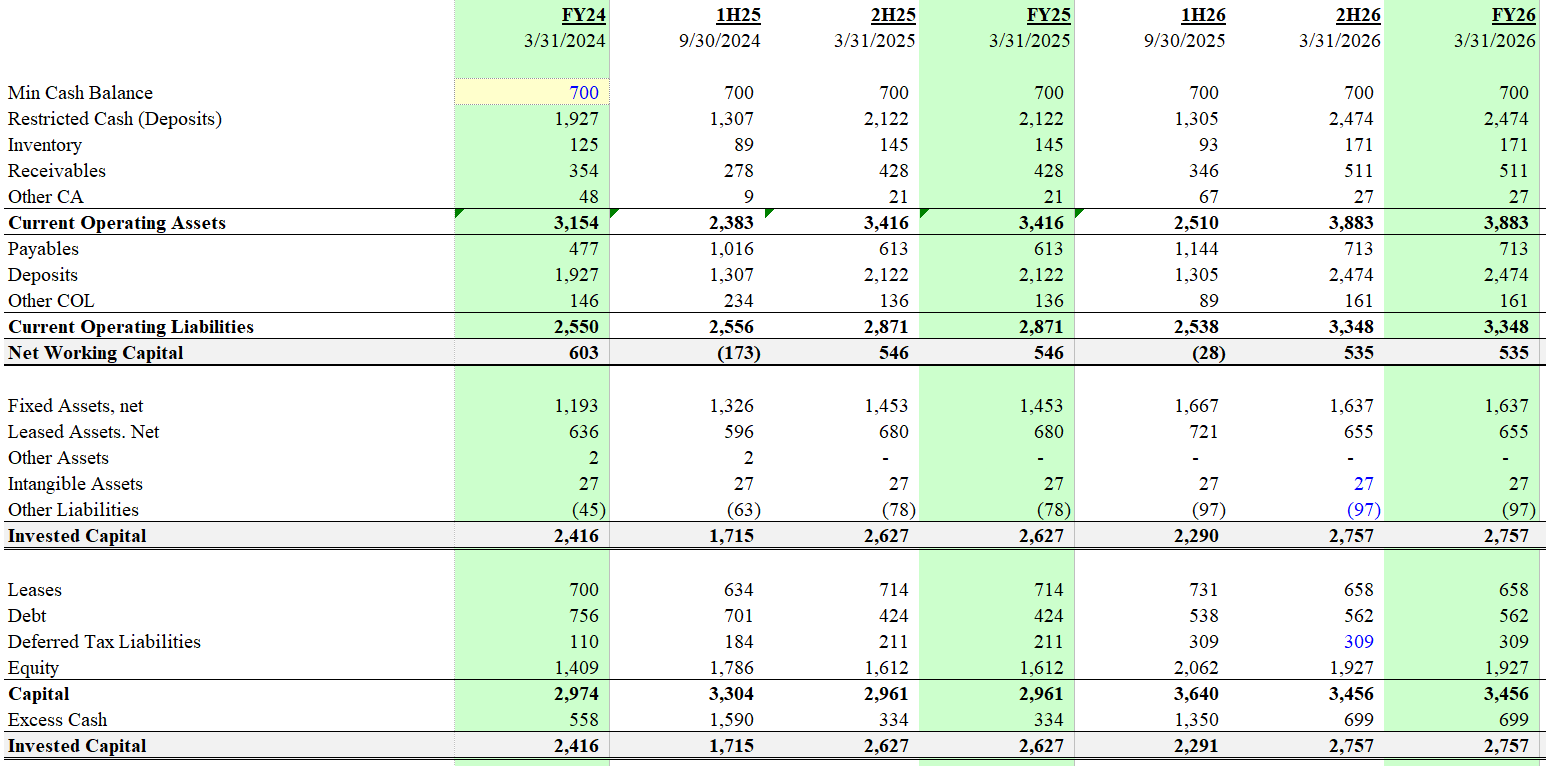

Including operating cash in invested capital, ROIC looks more like 13% (below) than the 15-17% noted in the Situation Brief. 13% ROIC isn’t bad for a hyper-competitive industry.

These reported returns are somewhat inflated by the age of their fleet, however. Sub 13% ROIC isn’t exactly the most exciting thing I’ve ever seen. Will the new planes be better or worse than that?

What’s the ROIC on the A321neo investments?

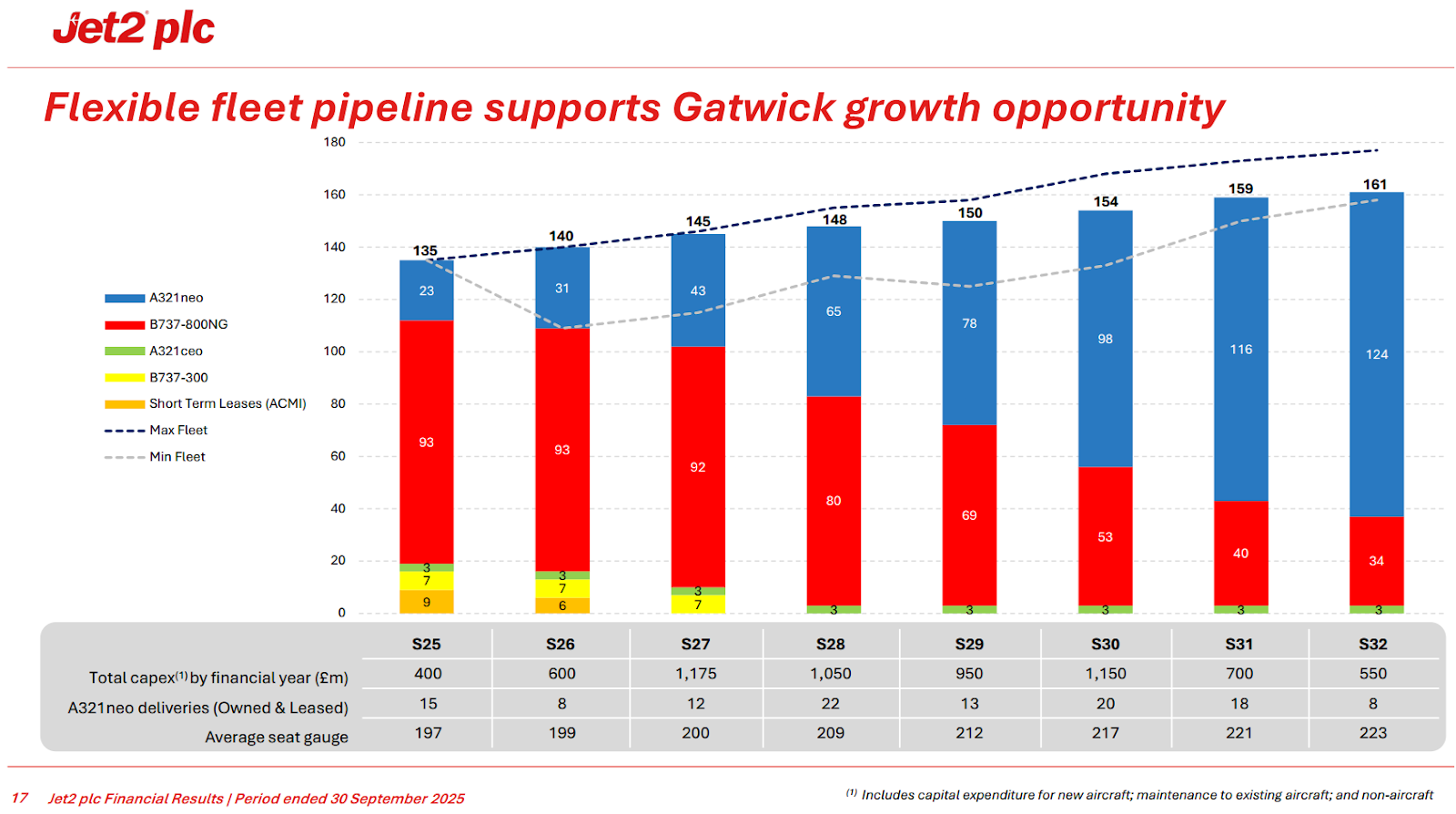

Jet2 is bringing in £450m in Net Income per year. Where’s it all going? Planes! Their fleet pipeline provides for 146 new owned and 9 new leased A321neo (neos) deliveries. The B737-800NG fleet will be phased out. Here is the latest disclosure:

A321neos have 232 seats vs. 189 on the 737-800s, so they create meaningful growth in seat capacity. I modelled this out and came up with the same Average Seat Gauge disclosed above, so I’m confident in these numbers. The fleet seat growth CAGR over the 7 years above is 4.4%.

The list price for neos is about $129m. Per Jet2’s Annual Report, they have a contract worth $16.7bn for 135 remaining neo deliveries--at list price. Only suckers pay list. Ballers pay £48m per plane. We can roughly triangulate this from Jet2’s disclosures.

Firstly, the slide above implies £55m per neo delivery, but it also includes all their maintenance and non-aircraft capex. So it’s less than that. We can look at gross adds to Aircraft PP&E, which was £740m in FY24 + FY25. Of this, £139m was pre-payments on future aircraft. £10-12m was for a new CFM LEAP engine. Take off another ~£50m or so on maintenance (guess). That leaves £540m for 14 deliveries, or £38m per plane. Assuming 80% of the total is due on delivery, that’s £48m per plane delivered.

Also, in 1H25, 2H25 and 1H26, they took out new JOLCO loans of £48, £99, and £191m to cover aircraft deliveries. JOLCO loans typically cover 100% of the purchase price of the planes. These are oddly close to exact multiples of £48m. It looks like they financed 1, 2, and 4 deliveries. So that triangulates.

Unit Economics

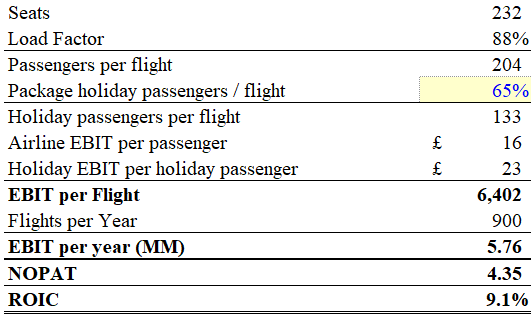

I wanted to know if these planes are good for shareholders. I calculated profits per passenger, passengers per flight, and flights per year for each neo. I’m not including all the fugly spreadsheets here.

In summary, it looks like a 9.1% ROIC per neo per annum. Accounting ROICs will improve over time, as revenue and opex are subject to inflation while the plane depreciates.

Assumptions

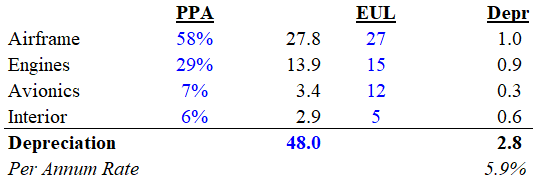

Depreciation: This ROIC assumes a £48m purchase price, with the £2.8m annual depreciation, as below:

Revenue and costs: For the purposes of analysis, I disaggregated profits into Airline and Holiday profits. (This nets out to total profits, so the division isn’t critical to the conclusion). Airline EBIT per passenger assumes current flight-only ticket prices for all customers. Direct costs per passenger include the neo’s fuel and carbon savings of £10 per passenger. I came up with £16 EBIT per airline passenger. The rest of the profits are attributable to the holiday package customers, who make up ⅔ of passengers. They add an extra £23 EBIT per flight per passenger from their holiday booking.

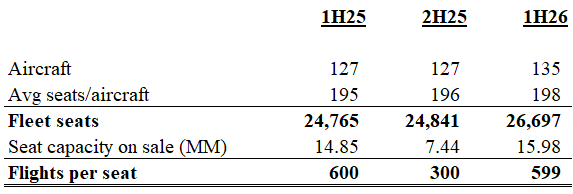

Flights per year: Their fleet size and average seat gauge shows that each seat makes 900 flights per annum (below) .That’s 2.5 flights per day on average - more than one return trip.

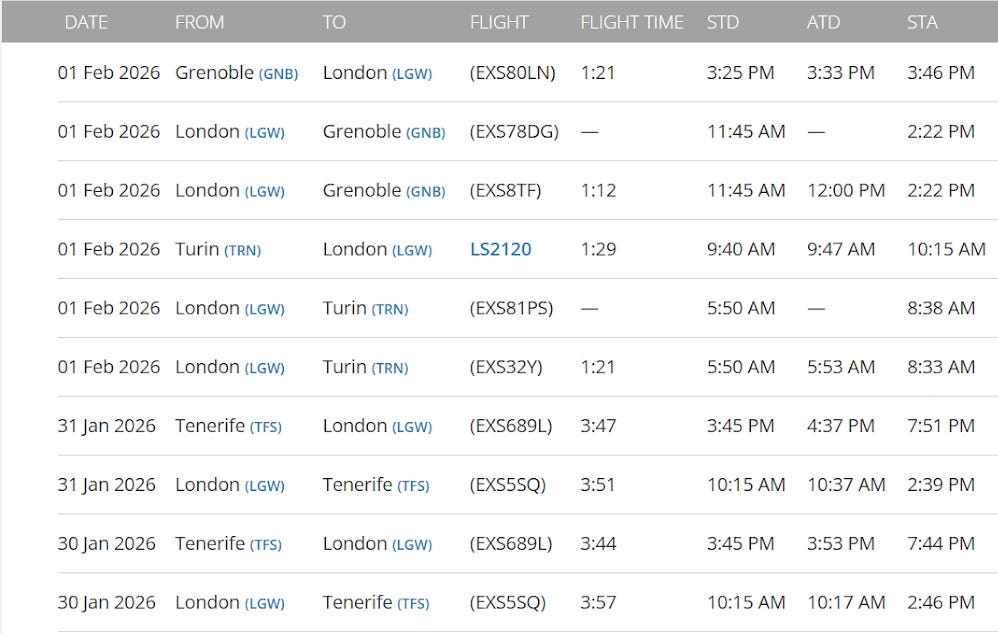

Here’s the flight log for one Jet2 A321 (tail: G-HLYF) stationed at Gatwick (below). On Feb 1st, it flew from London to Turin and back, and then London to Grenoble and back. 4 flights per day is doable when you’re only doing short haul. I pulled several planes’ tail codes and got the same result each time.

Updated Valuation

UPDATED: Valuation to include increased maintenance capex I don’t really focus on the value of individual stocks. I’m more interested in whether I’m getting a healthy economic yield, counting both the cash/distributable income today plus the economic value of reinvestments in growth. I intend to write a separate piece on this approach, but for now you’ll just have to trust that it reconciles with a traditional DCF or residual earnings model.

Updated: Jet2’s fleet plan includes a plan to replace the aged 737s with A321neos. The neos will, at least initially, produce lower ROICs than the depreciated 737s they replace. The capex plan implies that 6.5% of capacity will be scrapped annually for the next 8 years.

This capacity will be replaced with neos. As such, depreciation understates the upcoming “maintenance capex” required to maintain current production levels. Replacing depreciation with the capex needed to replace 6.5% of the EBIT with neos

Based on my analysis above, my base case for Jet2 indicates that the current £12.60 price offers ~18% economic yield. Fully valued, this is a price of ~£24. Depending on the competitive environment, I can see DCF valuations ranging from £9 to £30. However, I think there is liquidation value support below £12.

At what price would I be a seller? I’m not a fully diversified investor, so my required return is higher than the market. For a business like this--competitive, economically sensitive--I would require a 12% return. So as long as everything is going according to the base case, I’d likely hold until around £19.

I believe that a loss from current prices would necessitate a permanent decline in Jet2’s competitive position or industry-wide margins. We identified key two questions in the Jet2 Situation Brief:

Is their competitive advantage going away?

Is there a structural decline in industry margins?

I have some thoughts on these, but this post is getting too long. I will address them in a follow-up shortly.

If you enjoyed this post and want more, do me a favour and subscribe below. Please don’t make me beg. It’s very unattractive.

I’m new at this online publishing stuff. In my eagerness to get something out, I’ve made a mistake in my valuation logic. It’s going to bug the crap out of me all weekend, so I’m highlighting it here until I have a chance to publish a correction.

My valuation wrongly assumes maintenance capex ~= depreciation. Jet2’s current depreciation understates maintenance capex, as they are replacing depreciated 737 seats with new A321neo seats. The ROIC on the “existing” assets should be reduced to incorporate the increased maintenance capex.

Back of the envelope, the base case ROIC for existing assets should come down to ~10.5%. That changes current yield to ~15%, or fully valued stock price to £19.90.

***

There won’t be a big impact in the next year. From FY28 through FY31, however, the majority of new neos will be for replacement rather than growth. This will accelerate the drift of reported ROIC towards the 9% earned on new neos. It shouldn’t actually get that low, all else equal, because income inflation and asset depreciation will pull in the other direction.